Published in October 19, 2021

Credit Repair Companies: Are They Worth It?

In life, there’s rarely a quick fix. The same can be said for your credit score. You should be wary of any credit repair company promising to fix your credit score or repair your credit report in a short amount of time.

If you have found a mistake or an issue on your credit report, you might be trying to find out how to repair your credit report and, as a result, improve your credit score. During your search for answers, you may have come across credit repair companies. But what are credit repair companies and are they worth it?

Credit repair companies often promise to fix your credit score by fixing issues on your credit report for a fee. They usually promise fast results and high approval rates. Whilst this might seem like a great deal, unfortunately, the age-old saying comes into play here – if it sounds too good to be true, it probably is.

Credit repair companies in Australia

In Australia, there are a number of companies promising fast credit report repair or guarantee to fix your credit score in no time at all. However, we’re here to let you in on a secret – most of the quick fixes these companies promise to do are actually things you could do yourself, and for no cost whatsoever.

In some instances, however, there might not be a way to fix your credit score overnight. But, that doesn’t mean it can’t be done! As the saying goes, good things take time.

Should you use a credit repair company?

The tricks credit repair companies use to improve your credit report, are actually things that you can do yourself, and for free! So whilst a credit repair company might be able to improve your credit score and repair your credit report, you’re most likely just paying someone to do something you could do for yourself!

In the end, it’s always up to you. But, we’ve put together a short guide on how you can repair your credit report for free!

How to repair your credit report

Your credit score is an important number. It can be the difference between you being approved or rejected for a loan, a rental apartment, utilities and more. Your credit score is a 4-digit number ranging from 0 to 1,200. This number is based on your credit report which details information on your credit history – your credit accounts, credit applications, repayment history, defaults and more.

If you have a below-average credit score, then it might affect the loans and credit you apply for. Not only could a poor credit score result in you being rejected for finance, but it could also mean that you only have access to loans with higher interest rates and fees, which will cost you more in the long run!

1 in 5 credit reports contain some kind of mistake on them. These mistakes can damage your score. In Australia, you have a right to get any mistakes on your report fixed for free, and this is something you can do yourself.

Common mistakes on your credit report

Now you know that you can actually fix mistakes on your credit report for free, let’s take a look at some of the most common mistakes Aussies find on their credit reports.

Generally speaking, there are two types of mistakes made – those made by the credit reporting agency, which in Australia is either Equifax, Experian or Illion, or mistakes made by the credit provider. Your credit provider might be the company you have taken out a loan with, the bank that provided you with a credit card, or the financial institutions you applied for finance with.

When it comes to the credit reporting agencies, most often, they might have recorded your information incorrectly on your report, such as your name, date of birth or address. Furthermore, you might find that your debt – ie. a loan or credit card limit, has been listed more than once, or the amount of the debt is wrong.

When it comes to errors made by the credit provider, the Australian Securities and Investments Commission’s (ASIC) Moneysmart, highlights the following common mistakes:

- Incorrectly listed that a payment of $150 or more was overdue by 60 days or more;

- Did not notify you about an unpaid debt;

- Listed a default (an overdue debt) while you were in dispute about it;

- Didn’t show that they had agreed to put a payment plan in place or change the contract terms;

- Created an account by mistake or as a result of identity theft.

How to fix mistakes on your credit report

If you’ve taken a look at your credit report and you’ve spotted a mistake, what should you do next? If the change is about your personal information rather than about enquiries or accounts, then it’s likely a mistake from the credit reporting agency. You can directly contact your credit bureau and request a change.

If the mistake is regarding accounts or enquiries, you can contact your credit provider directly and ask them to change the entry. After investigating, the credit provider will then report back to the credit bureau and the change will become visible on your report.

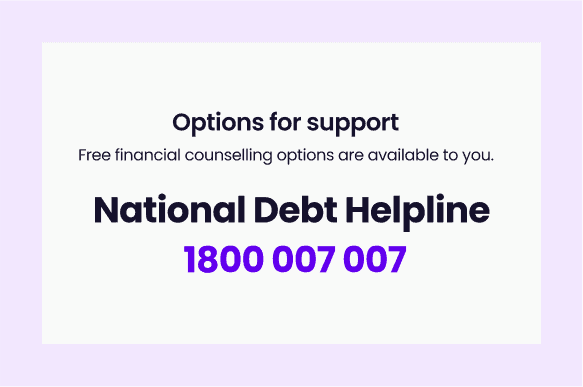

If you can’t resolve the issue, you can contact a free financial counsellor to mitigate, or directly reach out to the Australian Financial Complaints Authority (AFCA). However, you should try and solve this on your own terms first.

Improve your credit score

If your poor credit score hasn’t been caused by an error on your credit report, never fear! There are still plenty of other ways you can improve your credit score. We recently put together a quick guide to help you fix your credit score.

Before we give you tips on how to improve your credit score, it’s important to understand what goes onto your credit report and how long certain events stay on your report.

- Credit accounts – any open credit accounts and accounts that have been closed in the past two years

- Credit enquiries – 5 years

- Repayment history – for 2 years

- Defaults – 5 years

- Court judgements – 5 years

- Bankruptcies – at least 5 years

- Serious credit infringements – 7 years

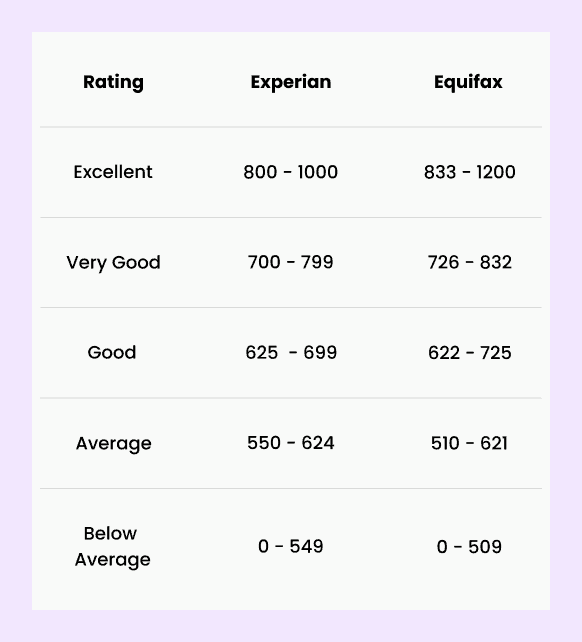

Want to know what is a good credit score? Here’s how Equifax and Experian categorise credit ratings in Australia:

Source: Experian and Equifax

Watch your credit applications

You might not realise it, but making multiple applications for credit, such as applying for multiple loans at once, can be damaging to your credit score. This is because each time you apply for credit the company you have applied to will check your credit report to see how risky of a borrower you are. This check registers as a hard enquiry on your credit report and can harm your credit score for a period of time. The more applications you make, the more damage you’ll do to your credit rating.

Not only will multiple hard enquiries lower your credit score, but it could also lead to you being rejected for a loan or other types of credit. Think of it from the perspective of a lender. You’ve just applied for a loan and they want to see if you’re a risky borrower. They check your credit score and see you’ve applied for multiple loans all at the same time. This could imply to them that you’re in financial distress, which means, you’re more of a risk. As a result, the lender could reject your application or provide you with the loan with a higher interest rate and fees – which will cost you.

Make your repayments on time

Your repayment history has a lot of weight when it comes to your credit score. This is because your rating is based on how well you can manage your debt. If you consistently pay your bills and make your credit repayments on time, then this is a clear demonstration that you are responsible with your debt, and therefore, a reliable borrower.

Let your credit accounts get old

This might seem strange at a first glance, but the age of your credit account can contribute positively to your credit score. The older the account, the better it is for your rating, as it demonstrates that you can consistently handle a line of credit.

Another way you can improve your credit score is by keeping your credit accounts open. Whilst we’re not advocating that you keep multiple credit accounts open just for the sake of it, you might want to consider keeping some open and in use so credit reporting agencies have data to base your credit score on.

Credit repair companies: are they worth it?

If you’re wanting to repair your credit report and fix your credit score, then this is generally something you can do yourself for no cost whatsoever. Because of this, whilst credit repair companies might be able to help you, anything that these companies are promising to do, are also things you could do yourself.

At the end of the day, the decision is yours. But it’s good to have all of the information on hand so you can make an informed decision. If you’re ever unsure, you can reach out to a free financial counsellor who can help you make the best decisions for your current situation.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

Subscribe to our newsletter

Stay up to date with Tippla's financial blog