Published in July 18, 2023

Why Is Your Credit Score Important? A Quick Overview

Whilst your credit score is only a number, it actually can impact your life in a very real way. So why is your credit score important? Tippla has the answers for you below.

What is a credit score?

Before we answer the question “why is your credit score important” it’s important to cover the basics first. What is a credit score? If you’re not sure what a credit score is – you’re not alone. In Australia, 73% of Australians don’t know their credit scores or why they are important.

Your credit score is a number ranging from 0 – 1,200. This number represents your creditworthiness (translation: how reliable of a borrower you are). The higher your credit score, the more reliable of a borrower you are perceived to be.

What is a reliable borrower?

A reliable borrower is someone who makes repayments on time. If a person takes out a loan, a reliable borrower would be expected to make their monthly repayments on time and during the length of the loan, completely repay their debt plus interest.

For a lender, a reliable borrower is seen as less of a risk, as they are more likely to repay the loan in full. A risky borrower, however, might miss payments, or default on their repayments. This means the lender could lose money if the borrower can’t repay the loan. A risky borrower would likely have a below-average credit score.

Who can see my credit score?

Your credit score is sensitive information. This means, not just anyone can see your credit score. You need to provide consent in order for a company to see your credit score.

So when does this happen? Every time you apply for credit – this could be a loan, credit card, phone plan or utilities, you are giving the company you are applying to permission to view your credit score and credit report.

When the credit provider looks at your credit score and report, they can judge how risky of a borrower you are, and determine what products they would be willing to offer you. If you have a below-average credit score, your application could be rejected.

How many credit scores do I have?

In Australia, there are three credit reporting agencies (CRAs) – Equifax, Experian and illion. Equifax and Experian are the two largest global CRAs. Each month credit providers report consumer credit information to either of these three agencies. The information these agencies receive from credit providers is what they use to calculate your scores.

Because of this, you have not one, but three credit scores in Australia. You have one each from Equifax, Experian and illion, and an adjoining credit report which holds all the information your credit score is based on.

What’s the difference between your credit score and credit report?

Your credit report holds all of your recent credit history. This includes any current credit accounts – loans, credit cards, utilities, phone plan, etc. It will also have your repayment history for the last two years, any closed credit accounts from the past two years, and any negative entries (defaults, bankruptcy, court judgements, etc).

Your credit score is a number ranging from 0 – 1,200. Your credit score is based on the information held on your credit report. If your credit report shows a good credit history, then you will likely have a high credit score. However, if there are multiple negative entries on your credit report, then your credit score will likely be lower.

How are credit scores calculated?

This question is a bit tricky because the exact algorithm credit agencies use to calculate your credit score is a well-kept secret. Not only that, but each of the three agencies calculates your score slightly differently. This means your credit scores can be different across the three agencies.

Nonetheless, we do know the general factors they consider when calculating your credit score.

These are the general factors used to calculate your Equifax credit score:

- The number of accounts you have;

- The types of accounts;

- The length of your credit history;

- Your payment history.

For Experian, the main factors it considers when calculating your credit score are:

- Type of credit providers that have made enquiries on your report;

- The type of credit you have applied for;

- Your repayment history;

- The credit limit of each other credit products;

- Negative entries;

- The number of credit enquiries (credit applications) you have made.

When is a credit score used?

Credit providers, such as banks, lenders and other financial institutions, use your credit score to evaluate whether they should give you credit or lend you money. They use your credit score to determine how much of a risk you pose and decide whether you qualify for a loan or credit, how much interest they should charge you, and how high your borrowing limit should be based on your credit history.

Why is your credit score important?

With all of this in mind – why is your credit score important? There are several reasons why which we’ve outlined below.

Your credit score can help or hinder your application

Your credit score can be the difference between you being accepted or rejected for credit. If you are applying for a large loan and you have a below-average credit score, the lender you’re applying with might determine that you’re too risky of a borrower and reject your application.

A good credit score, on the other hand, could boost your application. If you have a strong credit history, then a lender might look at your application more favourably and approve your loan application.

This is one of the reasons why your credit score is important.

Interest rates

The interest rates you’re charged when you take out credit can end up costing you a lot over the lifetime of the credit. That’s why it’s a good idea to try and find loans, credit cards and other credit products with lower interest rates.

However, whether you can access low-interest-rate products can be heavily dependent on your credit score. Why is this? Lenders and financial institutions use interest rates as a way of protecting themselves against risk.

If you are deemed to be a risky borrower, then you will likely only be offered products with high interest rates. That way, they get more money out of you quicker, so if you default on a repayment, they could already have a decent portion of the money they lent to you repaid.

This is another reason why your credit score is important – it can determine what products you’re offered and, if you have a good credit score, save you a lot of money in the long term.

Borrowing limit

Your credit score can also affect how much you can borrow. As with most things, it all boils down to risk. The bigger the loan, the bigger the risk could be for the lender should you default.

If you have a below-average credit score, then a lender might decide that it’s not willing to offer you a high borrowing limit and reject your application or only offer you products with lower borrowing limits.

However, if you had a good or higher credit score, then a lender could be willing to lend you larger amounts because you’re seen as less of a risk. This is how your credit score can influence how much you’re able to borrow.

What other factors do lenders look at?

It’s important to point out that your credit score is not the only factor that banks and lenders use to determine whether to lend you money. There are a range of factors they consider when making this decision. Nonetheless, your credit score is an important component of their decision.

Here’s what else they will likely consider:

- Your bank statements – credit providers will typically ask for your bank statements from the past three months. This way they can get an insight into your spending habits and savings so they can see if you are responsible with your money.

- Employment status and income – companies will want to ensure that you have reliable employment. Why? Because reliable employment infers that you are and will continue to receive regular income.

- Government benefits – if you rely too much on government benefits then companies might not be willing to lend you money.

- Gambling – do you gamble a lot? If so, this could be a red flag for lenders.

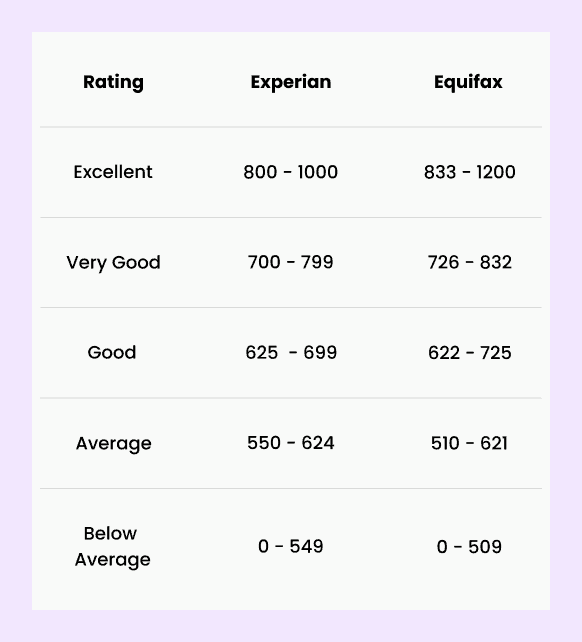

What is a good credit score?

A good credit score varies among the three CRAs. This is because they have different scales to rank your scores. Equifax measures your credit score on a scale from 0 – 1,200, Equifax, on the other hand, uses a scale of 0 – 1,000.

Here’s how they categorise your credit score:

Source: Experian and Equifax

How can you improve your credit score?

There are many ways you can improve your credit score. Here’s a quick breakdown to get you started:

1. Space out your credit applications

Each time you apply for credit, the company you have applied with will check your credit score. This is known as a hard enquiry and it lowers your credit score. Therefore, it’s a good idea to space out your credit applications.

Instead of applying for multiple loans and types of credit at once, you could instead do your research and make sure you meet the criteria before applying. You could also just make one application and wait and see if you are approved before going on to apply for other credit.

2. Make your repayments on time

Your repayment history contributes to a good chunk of your credit score. If you can show that you can make your repayments on time whenever you take on credit, then this will reflect positively on your credit report and boost your credit score.

On the flip side, if you miss your credit repayments frequently, then these will be listed as defaults on your credit report. Each time you default it will drag down your credit score. Not only that, but defaults stay on your credit report for up to five years.

This means each time you apply for credit in the next five years, every company you apply with will be able to see that you have previously defaulted on a payment. This will put you in the higher-risk category.

3. Check your credit report frequently

1 in 5 credit reports have some kind of mistake on them. This mistake could be an administration error, or it could be an indication that you’ve been a victim of identity theft.

Either way, mistakes in your credit report can harm your credit rating. That’s why it’s important to check your credit report frequently. That way you can identify a mistake early on and take the steps to remove the mistake.

4. Be consistent

Negative entries remain on your credit report for years. That’s why it’s important to be consistent with your good credit behaviour. One mistake can stay on your report for five years or more, and that mistake can affect your credit applications during this time. That’s why consistent positive credit behaviour can improve your credit score

The verdict: Why is your credit score important?

To sum everything up, here’s why your credit score is important:

- It could be the difference between you being accepted and rejected for credit;

- It can determine your borrowing capacity;

- It can affect the interest rates you’re charged (and either save or cost you money in the long term);

- It can impact what utilities and phone plans you can access.

Want to learn more about your credit score? Tippla’s credit school may be of great help! Simply sign up with us today to access our free resources that can give you further guidance about your credit score and ways you can build and improve it.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

Related articles

Financial Planning for Millennials

24/02/2025

In today’s fast-paced world, young adults face unique financial...

Navigating Credit Enquiries During Financial Hardships

15/07/2025

Credit enquiries, or credit checks, occur when a financial...

Understanding Payday Loans in Australia

28/11/2023

Payday loans are a type of financial tool that...

Choosing the Right Student Loan

29/12/2023

When it comes to pursuing higher education in Australia,...

Subscribe to our newsletter

Stay up to date with Tippla's financial blog