Published in February 24, 2025

Financial Planning for Millennials

In today’s fast-paced world, young adults face unique financial challenges. Understanding the significance of maintaining a good credit score is crucial for securing their financial future. As millennials navigate through the complexities of financial planning, it’s essential to equip yourself with the knowledge and tools needed to make smart financial decisions. By mastering essential financial strategies, you can pave the way for long-term financial success and stability.

What are your financial goals?

When setting financial goals, millennials need to consider short-term, medium-term, and long-term objectives.

Short-term goals may include building an emergency fund or paying off high-interest debt.

Medium-term goals could involve saving for a down payment for a home or funding further education.

Long-term goals often revolve around retirement planning and wealth management.

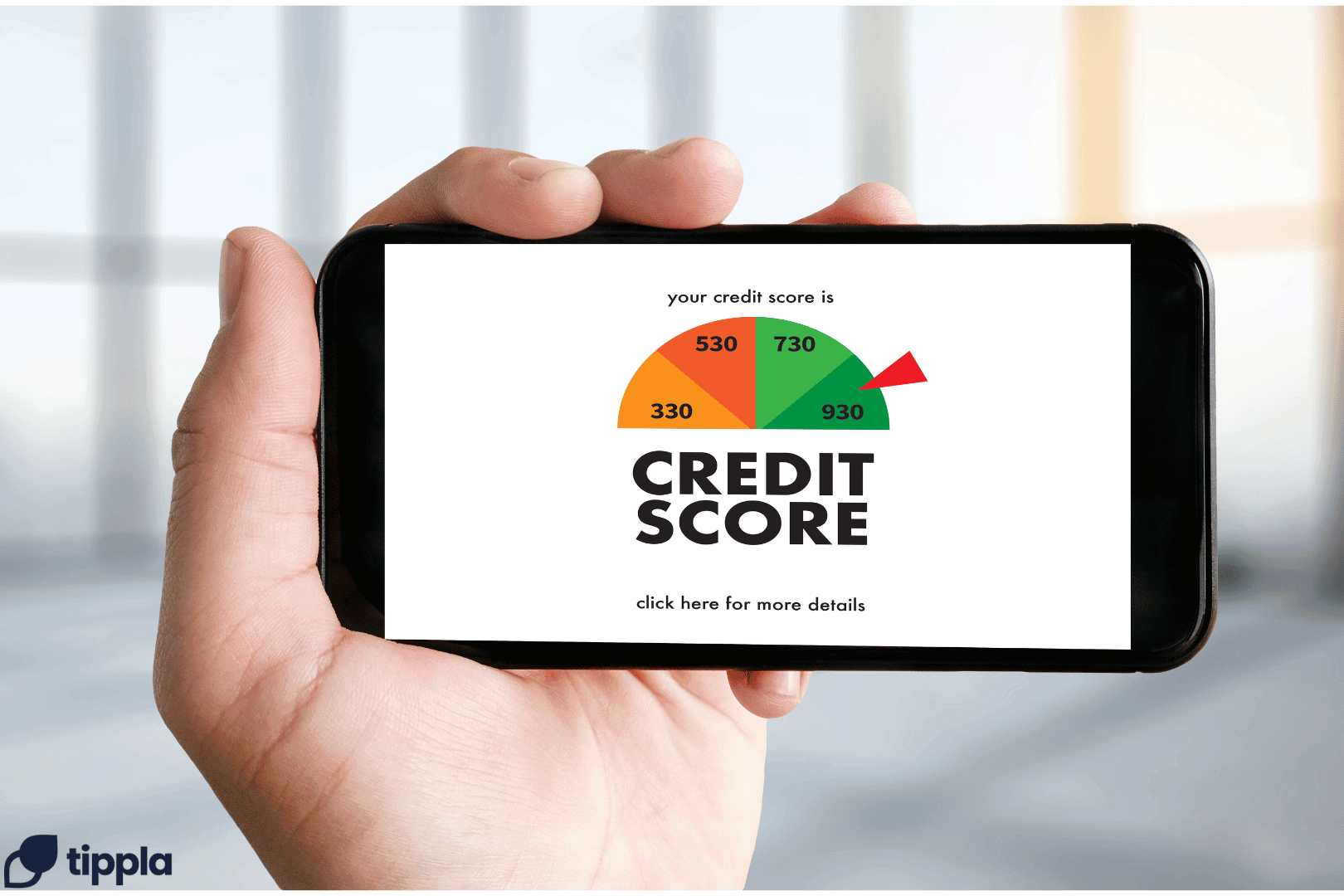

What is the status of your credit score?

Credit scores are numerical evaluations of an individual’s creditworthiness that significantly impact financial opportunities such as loan approvals and interest rates. They serve as a snapshot of an individual’s financial health and their likelihood of repaying borrowed funds. Understanding one’s credit score is crucial for making informed financial decisions and achieving long-term stability.

Helpful Tip 💡 You can start learning more about your credit scores through Tippla’s credit school. Monitor your credit score as often as you want, and the best part is it’s completely free. Simply sign up for Tippla today!

A high credit score significantly enhances the chances of receiving approval for loans from financial institutions, as lenders view a good credit score as an indicator of responsible financial behaviour. Individuals with a strong credit rating are more likely to qualify for lower interest rates on various types of loans, including mortgages, personal loans, and auto financing. Conversely, individuals with poor credit ratings may face challenges in securing loans at competitive interest rates, leading to higher borrowing costs and less favourable loan terms.

You can read more about credit scores in this related article:

- The Dos And Don’ts Of Credit: Protect Your Credit Score

- What’s the Most Efficient Way of Building Your Credit Score?

- Credit Scores for International Students in Australia: Building Credit History

Budgeting and Expense Management

One of the cornerstones of financial stability lies in the creation of a practical budget and the reduction of unnecessary expenses.

Strategies for Creating and Sticking to a Budget:

- Record Your Income: Start by documenting your sources of income. MoneySmart provides a step-by-step guide on how to do a budget, including setting spending limits and savings goals.

- Adjust and Iterate: Regularly adjust your budget based on changes in income or expenses. Flexibility is key to maintaining a realistic financial plan.

Tips for Reducing Expenses and Living Within Means:

- Identify Fixed and Variable Costs: Categorise expenses into fixed costs (rent, bills) and variable costs like groceries and transportation. This helps in prioritising and managing spending during a cost-of-living crisis.

- Emergency Fund: Establishing an emergency fund acts as a safety net for unexpected financial needs. It provides a sense of security and prevents individuals from falling into further debt during challenging times.

Managing Debt Effectively

- Consolidating High-Interest Debts: One way to tackle multiple debts is by consolidating them into a single loan with a lower interest rate. This can make repayments more manageable and reduce the overall interest paid.

- Seeking Professional Advice: Consulting with financial experts or debt counsellors can provide valuable insights into managing and reducing debt. They can offer tailored advice on creating a realistic repayment plan based on individual financial circumstances.

Basic Investment Options to Help You Get Started

Investing is a crucial aspect of financial planning as it allows you to grow your wealth over time, potentially outpacing inflation and helping you achieve your financial goals for the future. Understanding various investment options is essential. Below are some basic investment options, along with principles of risk tolerance and diversification:

Stocks

Stocks represent ownership in a company. Investing in stocks can offer the potential for high returns, but it comes with higher volatility. Beginners can start by selecting well-established companies with a history of stable performance.

Bonds

Bonds are fixed-income investments where investors lend money to a borrower (corporate or governmental) in exchange for periodic interest payments. They are generally considered less risky than stocks but offer lower returns. Bonds can provide stability to a diversified portfolio.

Mutual Funds

Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. They are managed by professionals, making them suitable for those with less investment knowledge. Mutual funds offer instant diversification, reducing individual stock risk.

Risk Tolerance and Diversification Principles

Understanding your risk tolerance is crucial. It reflects your ability and willingness to withstand market fluctuations. Diversification involves spreading investments across different asset classes to minimise risk. Balancing your portfolio based on your risk tolerance and diversifying across stocks, bonds, and other assets helps create a well-rounded investment strategy.

Should you get an insurance?

Insurance is also a crucial aspect of financial planning, especially for millennials as it safeguards your wealth and progress towards your goals by acting as a safety net against unexpected financial shocks. Here are some types of insurance millennials should consider and how to balance insurance needs with financial goals:

Health Insurance

Health insurance is an agreement where an insurance company commits to covering some or all medical expenses for the insured individual. This coverage is provided in exchange for a regular premium payment. Health insurance typically reimburses expenses related to medical and surgical treatments, offering financial protection against healthcare costs.

Life Insurance

Life insurance is a financial product that provides a payout in the event of the insured person’s death. Life insurance helps secure the financial well-being of the policyholder’s beneficiaries by offering a lump sum or periodic payments. It is designed to provide financial support, including covering debts, funeral expenses, and ongoing living costs for the surviving family members or dependents.

Complementing life insurance with funeral insurance can also provide a more comprehensive end-of-life plan to help ease the financial and logistical burden on loved ones.

Disability Insurance

Disability insurance in Australia addresses the financial challenges that individuals may face due to a disability. It offers protection by providing benefits to cover living expenses, rehabilitation, and other associated costs in case of a disability that limits the individual’s ability to work.

To strike the right balance, consider your financial goals, lifestyle, and risk tolerance. Evaluate the cost of insurance premiums against potential benefits. A sound financial plan ensures coverage for current and future priorities while achieving financial goals.

It’s Never Too Early to Think About Your Retirement

Planning for retirement early in life is crucial for financial security in later years. Understanding retirement accounts and recognising the importance of initiating savings at an early age are key aspects of a sound financial strategy.

Understanding Retirement Accounts

Superannuation

Superannuation is a compulsory savings scheme where your employer contributes a percentage of your salary (currently 11%) into a super fund on your behalf. Think of it as a long-term investment for your retirement income. You can also choose to make voluntary contributions beyond the employer’s obligation.

Generally, you can access your super when you reach your preservation age, which is between 55 and 60 years old, depending on your date of birth. There are specific conditions for early access to super in certain circumstances, such as severe financial hardship or terminal illness.

Types of Super Funds:

- Industry Super Funds: Not-for-profit funds with lower fees and a focus on member benefits.

- Retail Super Funds: Offered by banks and insurers, may have wider investment options but potentially higher fees.

- Self-Managed Super Funds (SMSFs): Allow greater control over investments but require significant time and expertise to manage.

The Importance of Starting Early

Starting retirement early holds immense importance, and the benefits compound over time. Here are some key reasons why:

Financial Advantage

- Compound interest: The earlier you start, the more time your contributions have to grow through compound interest. Even small monthly contributions can snowball into a significant nest egg over decades.

- Longer contribution period: Starting early allows you to contribute for a longer period, significantly increasing your accumulated amount.

- Reduced stress: Having a secure retirement fund relieves financial worry and stress later in life.

Lifestyle Benefits

- More flexibility: Early retirement allows you to pursue hobbies, travel, or spend more time with loved ones while you’re still healthy and energetic.

- Maintain your living standard: A well-funded retirement ensures you can maintain your desired lifestyle without experiencing financial hardship.

- Improved health outcomes: Studies suggest early retirees enjoy better physical and mental health due to reduced stress and increased leisure time.

Planning for Major Life Events

Planning for major life events like marriage, home acquisition, family start-up, career shift, or retirement requires careful planning because these decisions have significant and long-lasting impacts on your financial, emotional, and personal well-being. Over the next 20 years, Baby Boomers are projected to pass down an estimated $3.5 trillion in assets, marking Australia’s largest wealth transfer in history. It’s something many millennials are completely unprepared for.

First, set specific goals with timelines, considering both short-term and long-term goals. Evaluate your financial situation by analysing income, expenses, debts, and savings. Establish a budget and allocate resources judiciously. Gather information from reliable sources like government websites, financial institutions, and industry experts.

Build a strong support system by involving friends, family, and professionals. Be flexible and adapt to life’s deviations. Start planning early, prioritise spending, build an emergency fund, explore risk management strategies, and celebrate milestones. Remember that planning is a personal journey, tailoring your approach to individual needs and circumstances. With meticulous planning, dedication, and adaptability, you can navigate these life changes for long-term success.

Implementing these financial strategies can assist young adults in securing their financial future. By understanding the significance of maintaining a good credit score, setting clear financial goals, and exploring investment and retirement options, millennials can pave the way for long-term financial success and stability. Additionally, having a comprehensive financial plan in place for major life events provides millennials with a sense of security and peace of mind as they navigate through various milestones.

By acknowledging and addressing potential risks through thoughtful financial planning, millennials can safeguard their financial well-being while navigating through various life-changing events.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

Related articles

Building Your Credit Profile Early

01/09/2023

A Guide for Students and Young Adults Disclaimer: This...

9 Essentials To Have For Every Start-Up Business In Australia

11/07/2024

There’s no two ways about it: starting a new...

The Impact of Student Loans on Long-term Financial Planning

01/07/2024

Student loans, particularly through Australia’s Higher Education Loan Program...

The Ultimate Guide to Secure and Private Streaming

29/10/2024

These days, streaming has become a daily activity for...

Subscribe to our newsletter

Stay up to date with Tippla's financial blog